Using the Pension Fund to Close the City’s Budget Gap

We are excited to share insights from our economic policy team as they relate to the latest city news. David A. Lee, CNYCA's fiscal policy analyst, writes why Mayor Mamdani’s executive budget proposal to re-amortize the City’s pension system poses a risk for New York City’s future fiscal space.

Last Tuesday, Mayor Zohran Mamdani released his administration’s $124.7 billion executive budget. The executive budget will serve as our baseline through the final stretch of this year’s budget negotiation process through June 30th, which is the deadline for the Mayor and the City Council to ratify the budget.

Recall that in his preliminary budget, the Mayor unveiled a budget accompanied with a dire warning: that the City was facing a shortfall as extreme as $12.6 billion between fiscal years 2026 and 2027. Initially, the Mayor put forth plans to hike property taxes by 9.5 percent and withdraw $1.2 billion from the City Revenue Stabilization and Retirement Health Benefit Trust funds; these proposals have since been scuttered.

In the months since, between optimistic forecasts from City Hall of Wall Street windfalls that eliminated several billions of the projected deficits, and commitments from Albany, including a $1.2 billion allocation for expanding child care programs, the initial shortfall was whittled down the outstanding amount to $5.4 billion. The remainder is accounted for by the Citywide Savings Program, which identified $1.77 billion in savings from City agencies, including the cancellation of wasteful contracts and insourcing that work to City agencies, the levying of a pied-à-terre tax on non-primary residences with a valuation of $5 million or greater ($500 million), waiving the class size mandate on New York City schools ($508 million), and re-amortization of City contributions to the New York City Public Pension Funds totaling $2.3 billion.

As we await the final leg of the City’s budget negotiations, it behooves policymakers and engaged citizens to understand the comprehensive consequences of one of the more controversial of the Mayor’s cost-savings measures: re-amortization of City contributions to the pension system.

What are the New York City Public Pension Trusts?

Say you are a life-long public servant of the City of New York (thank you for your service!). While private sector employees are often enrolled in a 401(k) retirement plan, you, as a municipal worker, receive something better: a legal entitlement to post-retirement payments, accrued from contributing a portion of your paycheck into one of the City’s retirement systems throughout your career. Depending on your tier of retirement vesting, you are legally entitled to a monthly payout from your pension system for the remainder of your life.

The Administrative Code outlines the sources of contributions to three different types of pension funds: the annuity savings fund, which is financed by monthly contributions from City employees themselves, and the pension and contingent reserve funds, which are capitalized with direct contributions from the City. The Mayor’s Executive Budget proposes changes to the latter: the City’s contributions to the pension fund.

What is re-amortization?

Simply, it is changing the schedule on which payments are deferred.

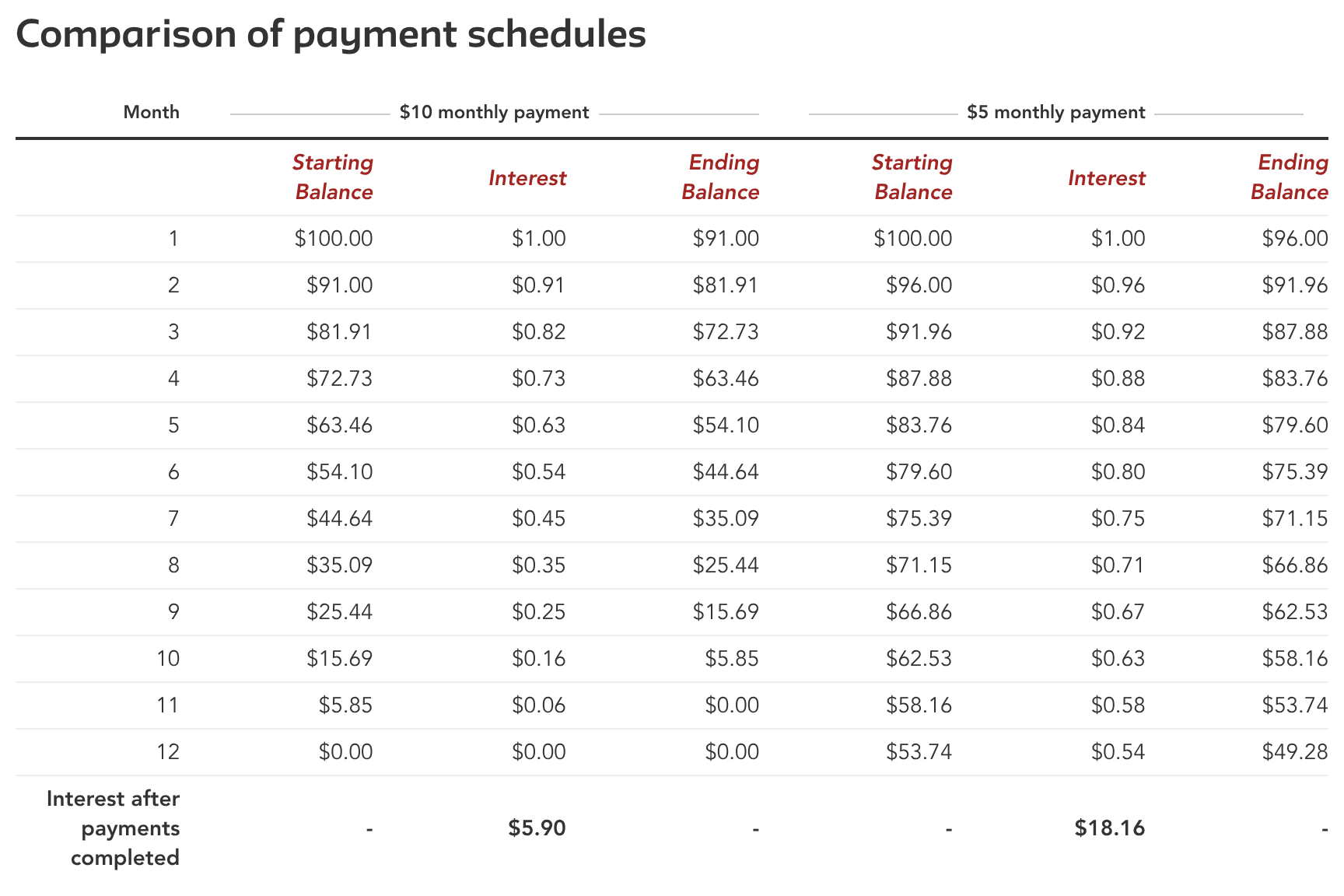

Imagine that you owe $100, and you opt to pay $10 a month to your creditor with a regular interest rate of 1 percent. In this scenario, it takes you 11 months to pay off the debt, with an additional $5.91 in interest on top of the original $100 principal. The trade off made in this decision was to accept a higher money outflow per month, but in exchange for less total money owed over the amortization schedule of this debt.

Now, consider the exact same terms, except you now pay $5 a month (see Figure 1):

Figure 1:

From only one variable change, it now takes two years to pay off the liability, with $18.16 paid in interest. By repaying less money per month, you traded off the ability to save more in the long-run. That is one choice of re-amortization. Two ways to make good on a debt, but contrasting trade offs in each decision.

The City’s pension trusts work similarly. The Office of the Actuary derives complex formulae that enable the City to accurately compute the valuation of the five pension trusts. Two integral pieces of information are fed into these actuarial models: the estimated lifespan of existing members, and the discount rate, or the future value of liabilities to pensioners in terms of present-day value.

To illustrate the concept of a discount rate, suppose that in 30 years you want $100 dollars. What amount of money and growth rate is needed to make that hand you want to convert that future $100 into its current value today? A 5 percent discount rate means that you could take $23 today, grow it at 5 percent every year for the next thirty years, and accrue $100 in the end.

Herein lies the problem: it is, naturally, impossible to perfectly prognosticate the future. Our knowledge of the distant future will always be limited. Discount rates are assumptions, encoded with expectations for what the future holds.

The intertwining of discount rate-setting and politics is a fascinating niche history in policymaking. For instance, an 8 percent discount rate on municipal pensions predominated throughout the 1990s, only for the double-whammy of the dot-com bubble and the Great Financial Crisis of 2008 to induce policymakers to downwardly revise these discount rates. Notably, then-Governor Andrew M. Cuomo in 2013 ratified a bill reducing the discount rate of the City’s pension trusts to 7 percent. The cost of the adjustment in assumptions was eased by allowing the city to re-amortize the unfunded actuarial liability, stretching the final payment till 2032. More recently, the Adams’ administration considered a re-amortization last year.

What does this mean for pensioners? The disbursements of the City’s pension system must ideally keep pace with increases in the cost of living. Conversely, it would be injudicious for the City to contribute excess funds to the pension at the expense of infrastructural and social service spending in the present. In particular, a balance must be struck to ensure that all anticipated and legally obligated liabilities to pensioners can be satisfied. When pension liabilities are unfunded, the City must be prudent with ensuring that the macroeconomic environment will be conducive for meeting these liabilities.

When will the City have Enough in the Pension Trusts?

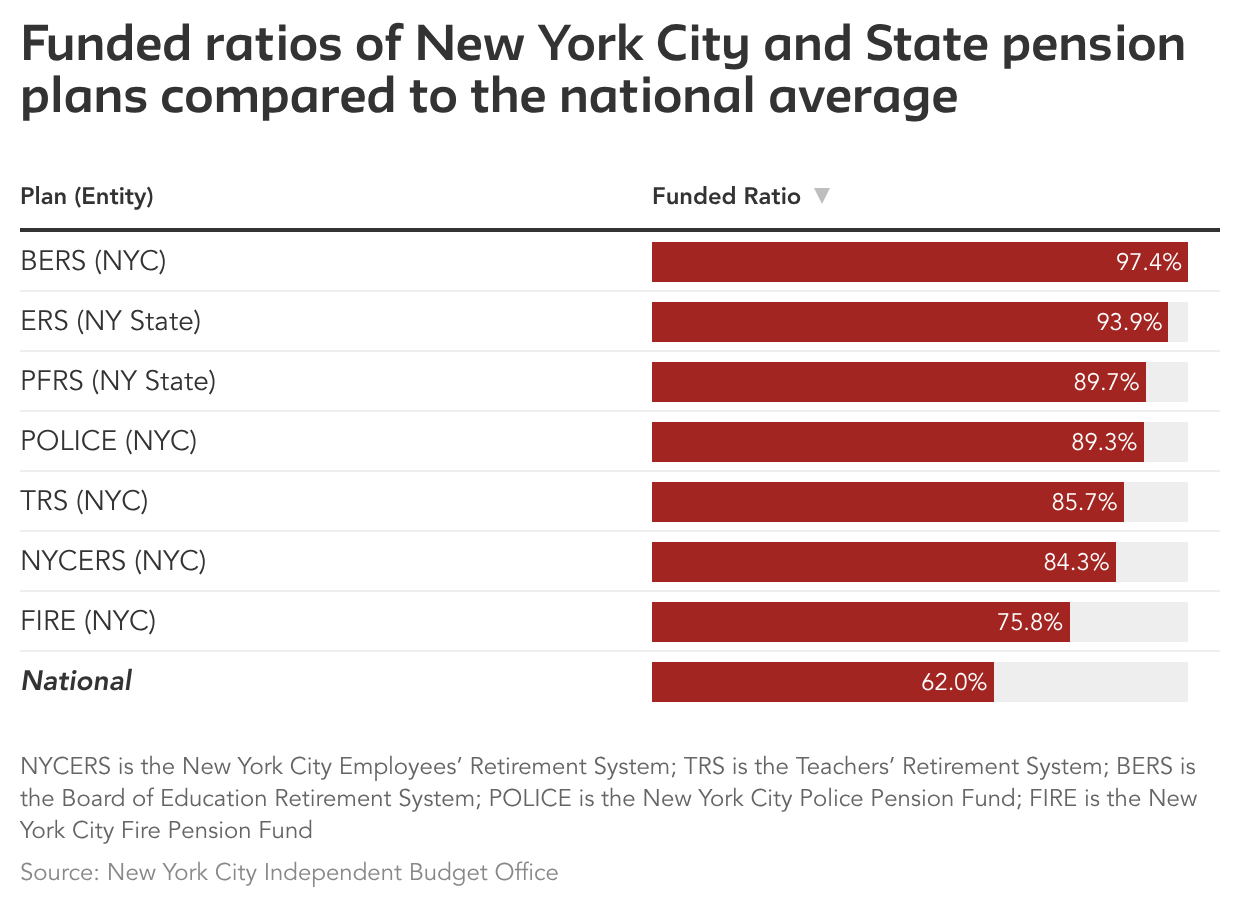

Last year, the New York City Independent Budget Office (IBO) published a report on legislation pending the State legislature regarding re-amortization of the NYCERS, TRS, and BERS trusts. In it, the IBO asks: when will New York City have enough in the pension trusts to satisfy all existing liabilities?

At the time of the publication, the IBO’s answer was 2032, at which point the “contribution cliff” kicks in. Upon fulfillment of the unfunded accrued liabilities (UAL), the remaining amount of liabilities to bring the pension trusts to 100 percent capable of meeting its funding obligations, the pension trusts would begin to owe a credit to the City, starting off as $961.3 million in 2033. For now, all of the City’s pension trusts have a majority of their liabilities funded, ranging between 75 to 97 percent (see Figure 2). But the remainder of the UALs needs to be obtained one way or another. Crucially, implicit in the assumptions behind the current amortization schedule is if the pension trusts meet their targeted investment return goals, for which there is never any guarantee. In light of the volatile macroeconomic environment the world finds itself in today, the Mamdani administration would be judicious to engage in restraint, not risks, with the pension trusts.

Figure 2:

By re-amortizing annual required contributions to a lesser amount, the City immediately would have freed up fiscal space with higher long-run interest service. Of course, it is far from the simplicity of switching from $10 to $5-a-month, nor is the re-amortization nearly as drastic. But the logic of the trade off is very real, and on the scale of New York City’s $124.7 billion financial plan.

The question we face is: how will Mayor Mamdani’s cost-savings plan for the pension system pan out?

Looking Ahead: The Symphony of New York’s Economy

Balancing the needs of the body politic against the macroeconomic realities the world faces requires absolute synchronization between a plethora of moving components, like a conductor directing a symphony orchestra.

But when done incorrectly, the harmony of the symphony disintegrates into cacophony. Undoubtedly, the Mayor’s plan is a non-trivial risk, and a gamble that can very well prove to falter. It is imperative for City Hall and fiscal policymakers to pay heed to a number of variables in play.

Intergenerational trade offs are at play by forcing future generations of taxpayers to bear the brunt of re-amortized pension costs.

Given that the trade off of lower monetary outflows today for higher costs tomorrow is at the heart of the administration’s proposal, City Hall ought to be mindful of the tax burden that it places on future generations of taxpayers.Proportionally higher interest service on re-amortized pension costs “crowds out” the City’s fiscal space to pursue the ambitious and expansionary agenda of the Mamdani administration.

Budgeting is necessarily a zero-sum endeavor: the opportunity cost of diverting more funds towards service on debt and accrued interest is funds that do not go into infrastructural and social service investment. Mamdani’s City Hall should be aware that deferring costs may “crowd out” the fiscal space to pursue the core of the Mayor’s signature proposals to expand services, like universal child care and free buses, none of which are fully funded in this year’s budget and will require significant future revenue.Will Wall Street windfalls persist?

Amidst widespread concerns of the impacts of AI on the broader economy, the war in Iran, and labor market woes facing new graduates, record-setting windfalls persist in Wall Street profits. Importantly, these windfalls are projected to sustain themselves for the foreseeable future by the Mayor’s Office of Management and Budget. But there is no Iron Law that bull markets remain bulls forever, and policymakers should not assume that good fortune in the financial markets will perpetuate indefinitely.Donald Trump and a dysfunctional Congress are constant institutional constraints until at least 2029. Albany is also likely to see constrained fiscal space in the event elevated state assistance to New York City continues to be warranted.

Cuts in federal aid to states and localities are no longer just threats made by President Trump; many have become a reality. Even if the Democratic Party succeeds in retaking one or both chambers of Congress in this year’s midterm elections, City Hall should assume that substantive federal assistance to buoy the City’s balance sheet remains out of the question for now. Fiscal space in Albany to provide support to the City should also not be taken for granted. Between proposals to reform Tier 6 of the state retirement system to closing major fiscal gaps in Medicaid and Essential Plan reimbursements – each amounting to billions of needed spending – City policymakers should not assume that current or additional increases in State aid are guaranteed.

The challenges facing this new generation of leaders at City Hall are as historic as the paradigm shift that has been ushered into the story of New York City. While there are concerns that the re-amortization could set the city up for extraordinary problems, there is also the possibility that prudent and responsive management and commitment to meeting obligations the city could manage. How the early savings would be used is also a critical factor in judging the appropriateness of going ahead with the re-amortization.

The Mayor who offered a promise in his inaugural address to overcome every moment of fiscal challenge with “ambition, not austerity” may well find himself in contradiction to that pledge.