Q: For Older Americans, What Does OBBBA Spell? A: Weaker Retirement Security.

As many of its major provisions take effect, the federal One Big Beautiful Bill Act (OBBBA) passed in 2025 is reshaping retirement security.

While a new tax deduction benefits a subset of higher-income retirees, the legislation blocks improvements to Medicare Savings Programs, introduces Medicaid work requirements for near-elderly adults, weakens nursing home staffing standards, allows enhanced Affordable Care Act premium tax credits to expire, and reduces support for the Supplemental Nutrition Assistance Program (SNAP). The net effect: weakened retirement security for older Americans.

Here are six graphs that tell the story.

Temporary Tax Relief for Some Seniors, Long-Term Costs for Social Security

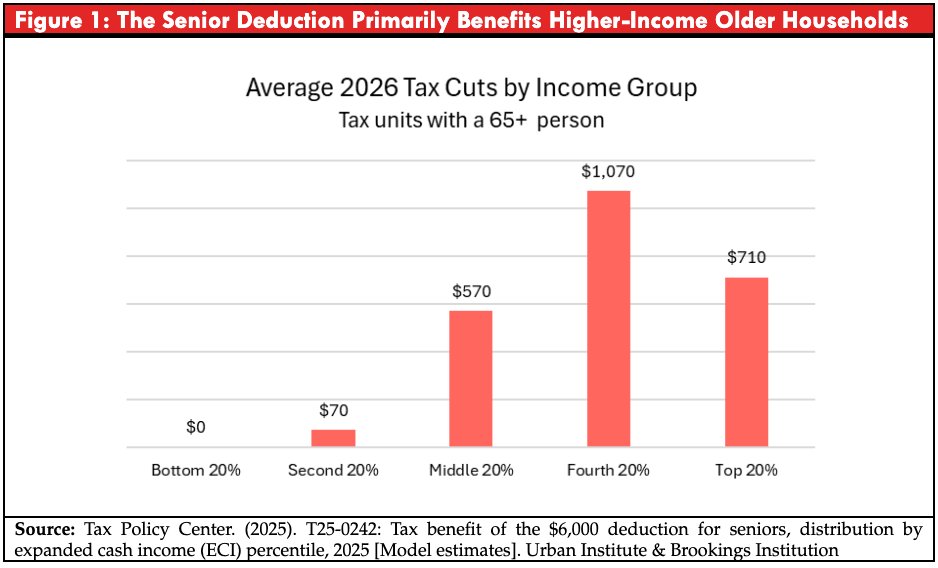

The OBBBA creates a temporary new deduction for taxpayers age 65 and older. Beginning in tax year 2026, seniors may claim an additional bonus deduction of up to $6,000 per person ($12,000 for married couples), on top of the standard deduction and existing age-based additions. The deduction phases out at higher income levels. It does not eliminate taxes on Social Security benefits outright. Instead, it reduces taxable income for some seniors, thereby lowering tax liability for those who owe income tax in the first place.

The Tax Policy Center estimates that only 46 percent of households with at least one person age 65 or older who file federal income taxes will receive any benefit from the provision. More than half of senior households will receive nothing. Among those who do benefit, the gains are concentrated in the upper half of the income distribution.

The deduction expires after four years. Yet its fiscal effects are not trivial. Taxes on Social Security benefits are credited to the Social Security and Medicare trust funds and are part of the programs’ dedicated financing structure, helping fund current benefits. By reducing the amount of Social Security income subject to federal taxation, the deduction shrinks revenues credited to the Social Security trust fund in particular, weakening its dedicated revenue base.

Medicare Affordability Is Weakened for Low-Income Beneficiaries

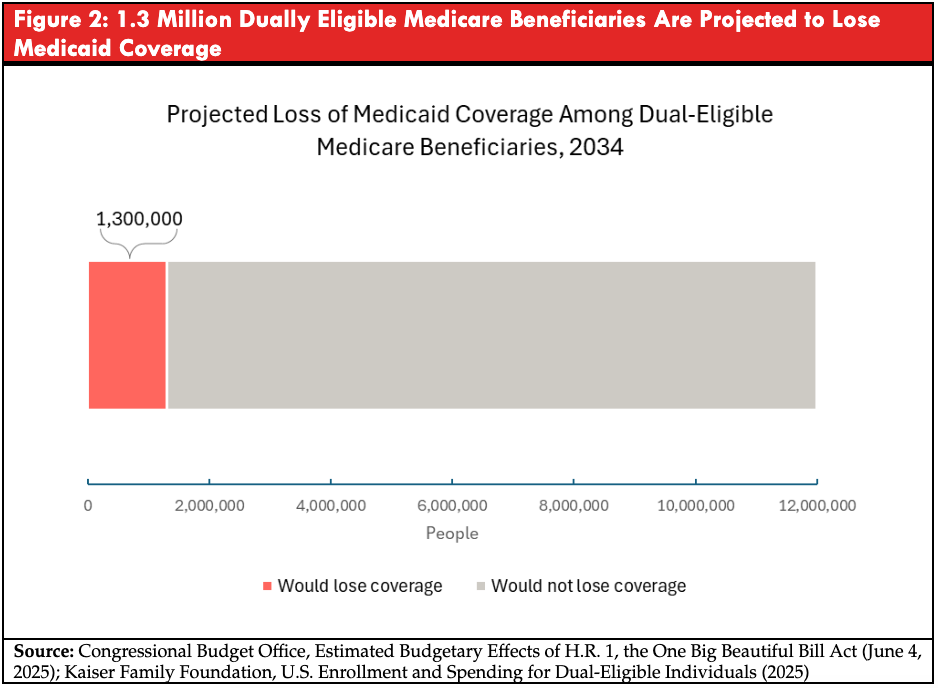

The OBBBA blocks implementation of regulations designed to streamline eligibility and enrollment for Medicare Savings Programs (MSPs). MSPs help low-income Medicare beneficiaries pay their Medicare Part B premiums and, in some cases, deductibles and cost sharing. For people with limited incomes, MSPs often determine whether Medicare coverage is actually usable, not just something they technically have but cannot afford to use.

The Congressional Budget Office estimates that approximately 1.3 million dual-eligible Medicare-Medicaid beneficiaries would lose Medicaid coverage and therefore assistance with Medicare premiums and cost sharing by 2034.

Medicaid Work Requirements and Weakened Long-Term Care Staffing Standards Increase Risk for Older Adults

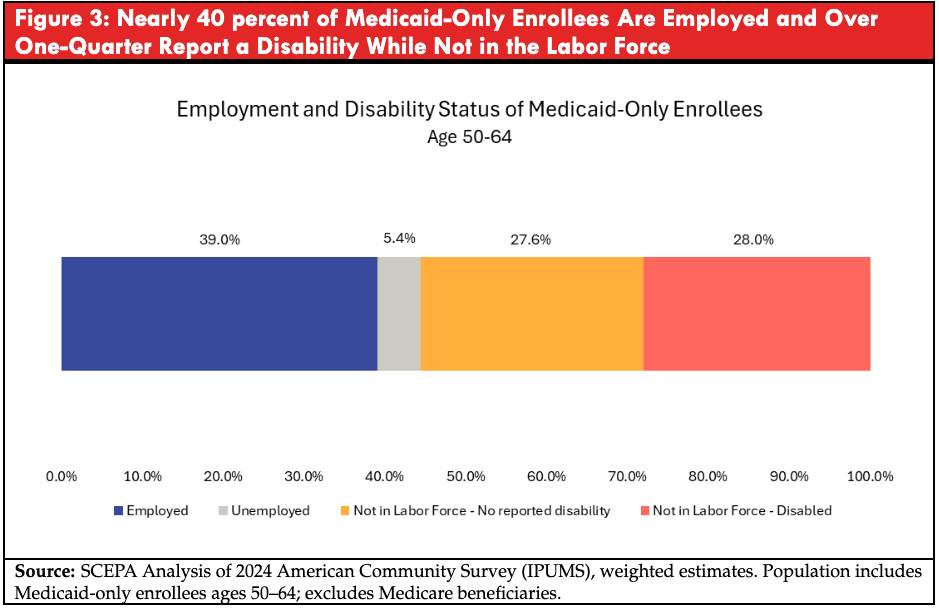

The OBBBA scales back Medicaid in ways that increase risk for older adults, particularly those ages 50 to 64 and those who rely on long-term care. Two changes are particularly damaging: the introduction of new Medicaid work requirements for adults up to age 64; and the blocking of updated nursing home staffing standards designed to improve care quality.

This figure underscores two important points. First, a substantial share of near-elderly Medicaid enrollees are already working. Second, a large fraction of those not working report functional limitations that may make consistent employment difficult, even if they do not meet formal disability thresholds for exemption. Work requirements in this context are less likely to move large numbers of older adults into stable employment and more likely to introduce additional administrative burdens for a medically vulnerable population with unstable work histories.

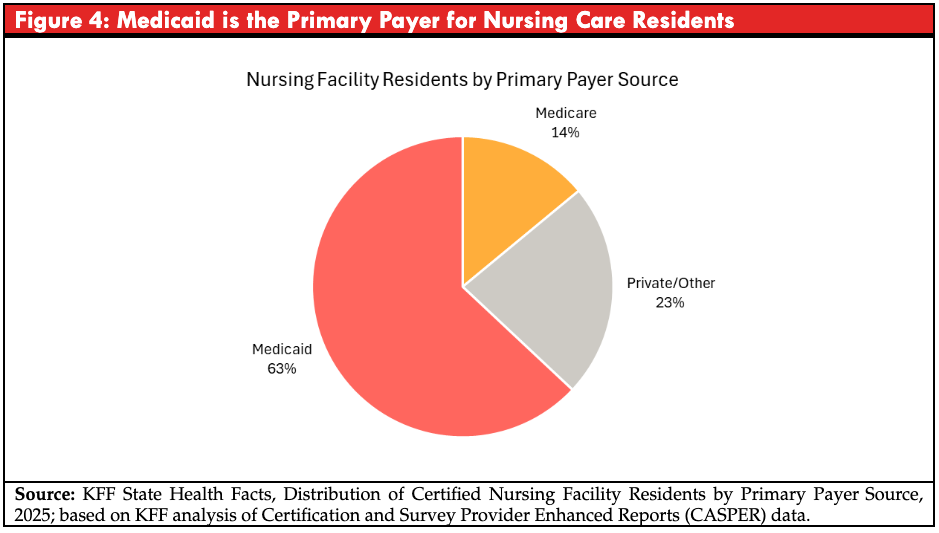

Because Medicaid is the dominant payer in nursing facilities, changes to federal standards governing Medicaid-participating facilities directly affect a large share of residents. Blocking enhanced staffing requirements does not reduce the need for care; rather, it alters the regulatory environment in which care is delivered. For older adults residing in nursing facilities, particularly those with significant physical or cognitive impairments, staffing levels are closely linked to quality of care, safety, and health outcomes. In practical terms, lower staffing levels can mean slower response times, reduced supervision, and higher risks of preventable harm for frail residents.

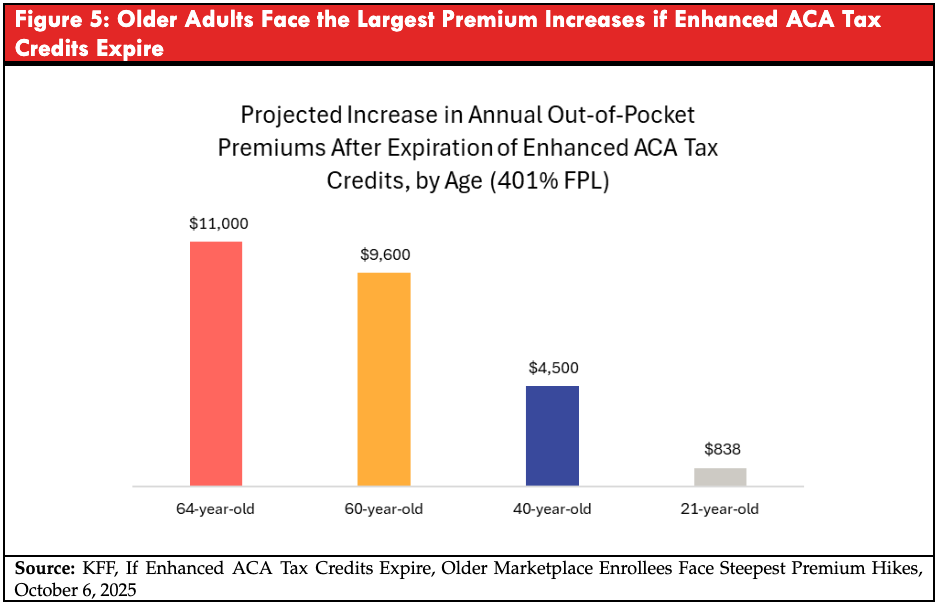

Expiration of Enhanced ACA Tax Credits Raises Health Insurance Costs and Reduces Coverage for Adults Ages 50–64

The enhanced premium tax credits enacted under the American Rescue Plan Act and later extended through 2025 reduced the amount that Marketplace enrollees were required to contribute toward their health insurance premiums. The policy lowered required premium contributions across all income levels, eliminated the “subsidy cliff” at 400 percent of the federal poverty level, and capped premium payments at 8.5 percent of income. As a result, many low-income enrollees qualified for zero-premium coverage, and middle-income adults, including those above 400 percent of poverty, became newly eligible for financial assistance.

Figure 5 illustrates the projected increase in annual out-of-pocket premiums for individuals with incomes just above the former subsidy cutoff.

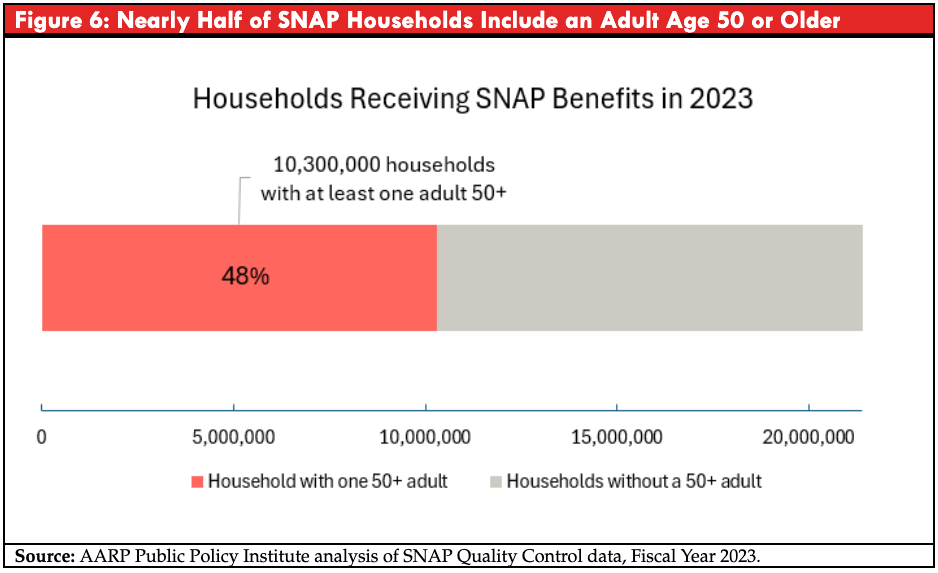

SNAP Cuts Increase Food Insecurity and Financial Strain for Older Adults

The OBBBA reduces federal support for SNAP, increasing the risk of food insecurity among older Americans. Nearly half of households participating in SNAP include an adult age 50 or older. Older SNAP households tend to have very limited incomes. Two-thirds have incomes below the federal poverty level.

The OBBBA expands SNAP work-reporting requirements to adults ages 55 to 64. Although described as promoting employment, many older SNAP participants face substantial barriers to stable work. In Fiscal Year 2023, 44 percent of SNAP participants ages 50 to 59 were estimated to have a disability, and many others experience unstable employment or caregiving responsibilities that complicate compliance with frequent reporting and recertification requirements. As with Medicaid work requirements, frequent reporting and recertification can themselves cause eligible individuals to lose benefits.

***

Taken together, these provisions shift retirement risk toward lower-income and medically vulnerable older adults while providing temporary tax relief to a narrower group of higher-income households. Although the law preserves the basic structure of Social Security, Medicare, Medicaid, and the ACA in name, it alters how those programs function in ways that increase economic and health insecurity for many Americans approaching or in retirement.

Strengthening retirement security will require deliberate attention not only to tax policy, but also to the affordability and accessibility of public programs on which millions of Americans rely as they approach and enter retirement.

Therefore, policymakers should: protect and strengthen Social Security’s long-term financing; restore and implement improvements to Medicare Savings Programs; repeal or significantly limit Medicaid work-reporting requirements for adults ages 50–64; reinstate and enforce strong nursing home staffing standards; reinstate enhanced Marketplace premium tax credits and eliminate abrupt subsidy cutoffs; and protect and stabilize SNAP access for older adults.

Drystan Phillips is a research fellow at the Schwartz Center for Economic Policy Analysis (SCEPA) at The New School and a New School PhD student in economics. SCEPA is headed by Teresa Ghilarducci, a New School professor of economics and policy analysis and a nationally recognized expert on retirement policy. This Urban Matters is adapted from a policy paper published earlier this month that is part of SCEPA’s “Tracking the Retirement Crisis” series.

Photo by: Socialsecurityoffices.info

{kind=link}